We should talk about risk …

Key concepts that shape how I think about risk

DISCLAIMER:

The article below is part of my “Summer Series”.

As I travel, I have pre-written these pieces to reflect on general trading experiences through a lens that I believe may be of interest.

TLDR - Key takeaways

Risk management comes first, always

Before returns, narratives, or entry points, the priority is avoiding risk of ruin. Position sizing, diversification, leverage, and aligning risk with your personality and time horizon matter more than being “right.”Anything can happen: prepare for tails

Influenced by Taleb’s first book, I engrained the following in my investment and trading process: markets are dominated by randomness, fat tails, and rare events. “Never” and “always” are red flags. Successful investing and trading require humility and structures that survive extreme outcomes.Biases silently sabotage decision-making

Cognitive biases (overconfidence, action bias, aversion to loss, recency bias, etc.) systematically distort judgment. The antidote is awareness, a repeatable process, deep research, and continuous self-reflection.Returns follow good downside control

Whether trading or investing, focus on asymmetric risk/reward. In trading, this comes via stop losses; in investing, via margins of safety, thesis discipline, sizing, and diversification suited to your temperament. Control the downside and let the upside look after itself.

INTRODUCTION

This article is not about an investment idea that you could dig into.

It is, rather, about a few principles that have guided me in my trading career and that also apply well to the investment process.

I find them worthwhile, and I hope you will too.

WHAT IS RISK MANAGEMENT

In investing, risk management is defined as the process of identifying, measuring and controlling potential losses so that you can stay invested long enough to achieve your financial goals.

It typically encompasses:

position sizing1.

diversification.

setting stop losses.

managing leverage.

aligning risk with your time horizon and personal preferences.

That last point is often overlooked but is central to success: in order to achieve great results, one needs to spend time filtering through what works and what does not in relation to their own personality.

If you have ever been responsible for a trading book at a financial institution, you quickly realise that, if you manage to hold on to your seat long enough, risk management comes before everything else2.

I like to see risk management as an umbrella that covers all other elements of the investment or trading process.

Therefore, in my framework, risk management comes first.

The reason it is paramount: we need to do all we can to avoid risk of ruin3.

Put differently: what is the point of dreaming about making a fortune (i.e. contemplating reward) if you can't play ?!

Ok, enough with the various angles to illustrate the concept.

I think it is pretty clear at this point.

Let me now turn to my approach to risk and Taleb’s influence on it.

BLACK SWAN AND OSTRICHES4

A trading floor can be very professional, operating at the cutting edge. If you were to visit one for the first time, you could really understand why “retail” cannot compete in some circles. Here, I refer specifically to trading, not investing5.

Yet, at the same time, after years of experience, I found that many professional traders can seem out of touch and may not fully consider how much uncertainty affects their results.

In 2005, ex-derivatives trader Nassim Taleb published Fooled by Randomness. His book is about understanding the hidden role of luck, probabilities, and rare events in life and markets, and why one should cultivate humility and risk awareness rather than overestimating skill.

I think some concepts in his first esoteric6 book had a huge impact on me.

The key principles he tackled are:

Luck vs. skill: humans often mistake luck for skill, especially in finance

Consequence: be cautious!

Survivorship bias: we focus on winners and success stories while ignoring the vast number of failures.

Traders often underestimate fat tails: this leads to risk MISmanagement.

Randomness affects all aspects of our lives. Nassim stresses humility, i.e. accept that outcomes are partly beyond our control.

Concept of the Black Swan7: a rare and unpredictable event with massive impact that people tend to explain away as obvious only after it has happened.

People fail to consider what could have happened that did not.

My main takeaway from the book was that anything can happen.

Never say never, and trade or invest accordingly.

I was told many times that certain events could not occur in the markets I traded. Yet they did8.

Once I understood that, my whole approach to trading changed.

One example (apart from preparing for large moves on some products that were left for dead), was how I came to deal with weather variability.

I traded Power and Gas for 15 years, and weather had a huge influence on price movements. Especially short-term tenors, but not just. Yet, as you know, weather forecasts are very volatile.

I therefore gradually started to use weather derivatives when it was possible9.

And I used the pricing of weather in the power market to my advantage: I focused my trading on the times where this pricing gave me an asymmetric advantage10.

Also, because of it, I see red flags when I hear people talking about investing or trading using words like “never” or “always” - anyone speaking in absolutes really …

At a high level, my conclusion is:

- Focus on risk management first.

- Prepare for rare events.

The reason we fail, as mentioned in the bullet points of Taleb’s book, are linked to biases.

Let’s discuss what those are.

COGNITIVE BIASES AND HOW THEY MAKE US SEE THE WORLD

The study of cognitive biases was pioneered primarily by Daniel Kahneman and Amos Tversky (authors of the now-renowned Thinking, Fast and Slow11).

The two psychologists, who worked together in the 1970s, changed how we understand human decision-making under uncertainty. Their work showed that human decision-making is systematically flawed in predictable ways.

They demonstrated that:

- Humans rely on heuristics (mental shortcuts to make decisions quickly).

- These heuristics systematically lead to predictable biases (systematic errors resulting from relying on these shortcuts).

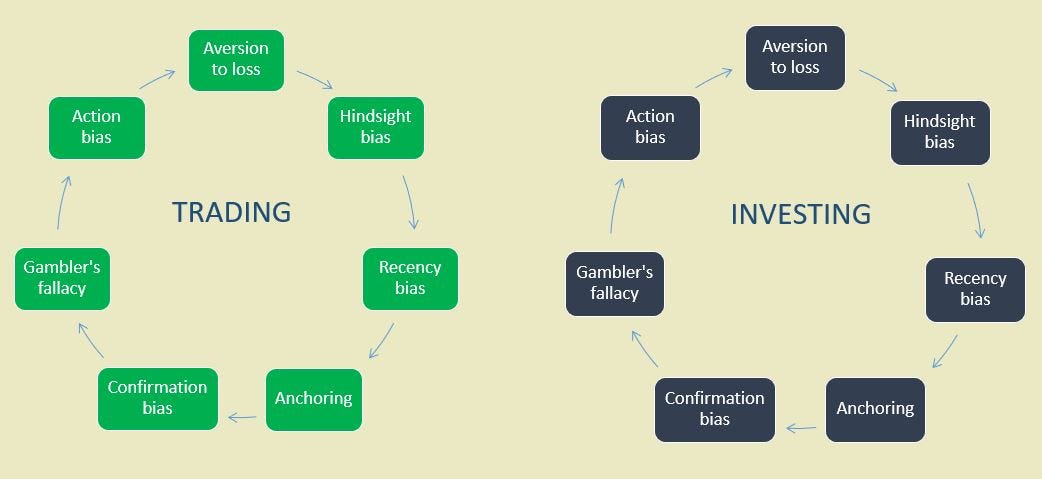

A summary of biases relevant for trading and investing could be:

Comments on my diagram:

I had made list for both processes in the past. As you can see, there is a lot of overlap. I am not even saying they don’t completely intersect. Maybe recency bias is less relevant to investing -- but that remains to be seen.

Loss aversion is less an issue in investing, in my opinion (especially due to leveraging in trading, which can wipe you out quickly …).

Gambler’s fallacy is much more relevant to trading.

Action bias (i.e. overtrading) is a common sin in our communities!

How do we improve and inflect our instincts to be better investors …

Recognize that biases exist.

Work continuously on a process (this is massive to me). It does not have to be automated or quantitative, qualitative approaches can also work. The more you practice investing, the more you develop a process. I have a pretty clear one now, albeit not necessarily written down, but I can explain it.

Deepen due diligence to focus on facts rather than narratives.

Be open-minded. When combined with deeper research (as per point 3), this allows you to debunk strong narratives that, upon closer examination, can often be completely unrealistic. It also helps overcome overconfidence.

DYOR (Do Your Own Research, see more at the end) helps you understand your personal parameters, notably your tolerance for risk, and allows you to manage your risk aversion.

DO NOT TAKE MY WORD FOR IT: ASK THE MARKET WIZARDS

I feel like I cannot finish talking about risk without mentioning the fantastic book written by Jack Schwager in 1989, Market Wizards: Interviews with Top Traders which is, for me, the greatest book ever written on trading.

It captures well what risk management is about, and you should definitely read it if you have not.

Caveat: it is more about trading than investing.

What is noticeable is that many comments from different interviewees overlap. Given their stature, I think it is worth making a four-point recap of the most important lessons related to my post today:

risk control is not optional.

find a style that fits you.

don’t focus on trades you don’t believe in.

careful with overleveraging after wins.

And this quote from Paul Tudor Jones, “Losers average losers”.

RISK CONTROL DOES NOT STAND ALONE: ENTER RETURNS

How does this whole downside-appreciation exercise relate to the reward aspect of investing?

As mentioned in Hated you say ?:

“I am fairly flexible where I go and how I allocate my investments.

But the basis is to control my downside.

I guess 15 years of prop trading Energy had its influence …

For me it's all about risk/reward.

As long I can control the downside the upside should take care of itself.

It's not so far away from the concept of margin of safety from value investing, as advocated by Benjamin Graham. Just another angle.

This paragraph sums it well for me.

This is the gist of how view upside potential relative to all the risk control processes I have described in this article.

I also think it’s important to make a further distinction between investing and trading here.

In Trading, you can achieve a significant skew between risk and reward, as long as you have a robust stop-loss process in place.

For investing though, as we lengthen our time horizon and decrease or eliminate the use of leverage, we likely do not use a formal stop loss.

Yet, even without it, I see risk as “controlled” as long as I stick to the following:

When fundamentals (i.e. the thesis) change in a way the investment is no longer valid, I either reduce or exit my position altogether.

I have margins of safety in the form of cash flows, yields, asset trading below my calculated liquidation-value: these provide a real floor or compensation for what I own.

I carefully manage my position sizing and diversification12.

CONCLUSION

NO DYODD today … but an exercise I would recommend to everyone is to reflect carefully and continuously on what risk means to you.

Which time horizon are you best suited to, and which suits you best ?

Which investment process defines you most clearly ?

In some way, the DYOR (no, not that luxury brand): Do Your Own Reflection …

Okay, on that little pun, thank you for reading.

Fred

This is very well highlighted by fantastic Fixed-income trader Harley Bassman, who he ends all his letters with: "Sizing is more important than entry level”.

When trading for large firms, I saw time and again how traders (and I include myself) form very strong beliefs about a thesis that then gets disproven and causes large losses. Unless you are prepared to bite the bullet and cut or reverse in some cases, you are done. Literally. While it is NEVER easy to take the losses, experience helps you act faster in those situations. And the faster you are out, the better it is for you in general.

Chance that losses drain your capital so much that you can't recover or continue investing.

Yes, because ostriches are one of the few animals that choose, in an unhelpful way, to ignore danger!

I understand that retail can have the upper hand in a few rare instances, as exemplified by GameStop or buy-and-hold versus benchmark managers. But when it comes to trading, in the vast majority of cases, it simply cannot. So I focus mostly on trading here, not investing.

The author takes many detours, veering into philosophy and Epicureanism, which can lose the reader at times, as I experienced upon re-reading it recently.

Yes, before Black Swan became a book in 2007, Taleb touched upon the concept in Fooled by Randomness.

Whether it was Oil not trading below 70$ anytime soon in mid-2014 - a bet I won with our head of trading. Whether it was the coal traders at my old shop telling me I was crazy for buying OTM call options on coal against a top trading house, for peanuts, betting on a large upward move in the years ahead. Or more recently, why I was buying solar stocks in 2024/2025 !

I stopped trading Power in 2020 as a PM, so I cannot speak about recent developments. But when I was active, Weather Derivatives were highly illiquid instruments. They were mostly transacted on a bespoke basis by specialists in the OTC markets. Furthermore, there were only a handful of times per year where it was worth entering into such a structure. But when it was, the skew between risk and reward was terrific. I still did not find many traders in my industry who were very keen to use them, though. I guess they were happier than me to bear the weather variability …

This comment relates to trading short-term power. It often meant taking a contrarian position: for instance betting on higher power prices when wind forecast was forecasted to be very high. If my calculations were correct and it was priced in (or even too bearish despite record wind generation expected), I would make money regardless of high renewable generation occurring. And if less wind actually showed up, then a large profit would be made.

It was written by Daniel Kahneman, but since Amos Tversky had passed away, it is seen as a posthumous recap of their combined work.

It is well explained by the GOATS (Buffet, Druckenmiller) that diversification can be the enemy, and a concentrated egg basket is better than having many eggs, as long as you watch them very carefully. I agree. Another way to look at it is, the more you investigate an investment, the more confidence (objective confidence !) you hopefully acquire regarding its limitations or potential greatness. We are NOT all (and by definition, almost no one) the Goats. Hence, diversification is truly important in my opinion. Secondly, it is very personality-dependent. As I have improved my investment process, I have greatly increased concentration. But only up to the point where I am comfortable relative to the total downside, i.e. I almost always contemplate the possibility that a given asset could go to zero …

How do you manage gaps that pierce through your stops?