Hated you say ?

Sun is started to shine again on this deserted sector

Up until Q3 of last year, solar was a hated sector.

Investors were shunning it.

And “Energy” aficionados on Twitter/X constantly vilifying it.

Oil, Gas and Uranium … yes, super bullish.

But that part of the retail crowd tends to treat wind and solar like it’s the second worst thing behind the plague.

I find it silly.

First, I witnessed first-hand how well renewables can get integrated into power systems at large scale, being involved in European wholesale markets during 15 years.

And second, quite importantly as an investor, there is political will behind it.

As one of my favourite trader/investor The MacroTourist, Kevin Muir, likes to say “trade the market in front of you, not the one you wish you had” !

I have had large Uranium positions this decade. I think Gas as a technology is a must and have traded it actively. And Oil producers represent currently north of 10% of my stock portfolio.

Yet, I have been quite fond of solar as an investment since Q2 of 2024.

All that to say, I am agnostic in term of what Energy I invest in.

WHY THIS INDUSTRY ?

What picked my interest a year and a half ago, was how much renewables equities had corrected. The best benchmark to me is the ICLN ETF (Ishares Global Clean Energy trading on Nasdaq).

It was down a whopping 60% from the 2021 highs by the middle of 2024.

For some time I had found many Cleantech companies to be outside my comfort zone. Way too expensive value wise, and or not making money.

But I like a good deal, and the above chart looked pretty gloomy then.

It made me investigate.

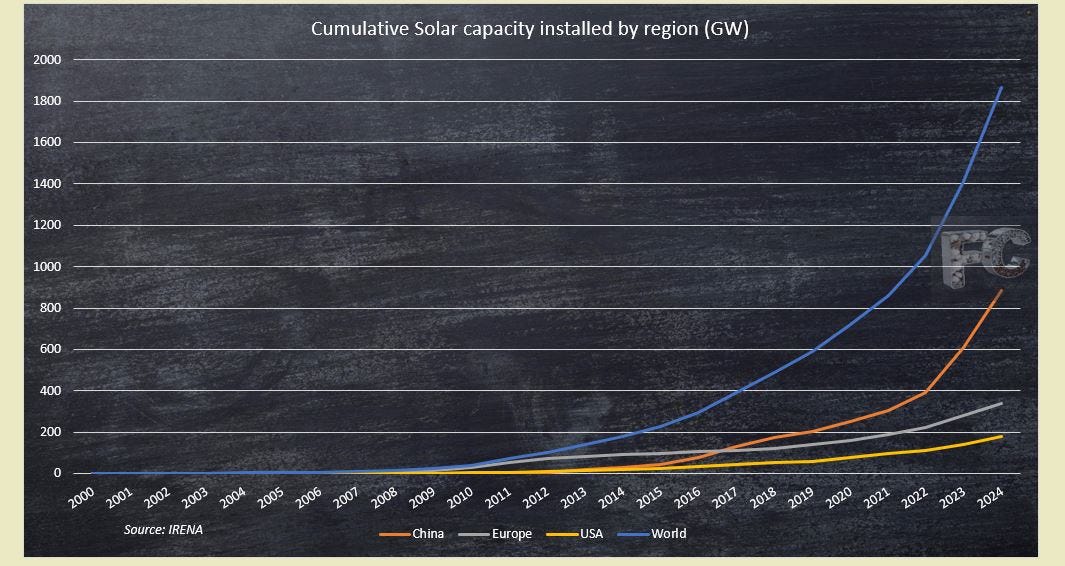

One of the things that blew my mind when looking further into the industry, was when I came across the absolute breathtaking pace at which capacity was being installed worldwide.

I had witnessed it first hand in Europe. But I did not keep a close eye on what was happening elsewhere in the world.

China had gotten busy (!), and many other countries were seeing large growth (India, Brazil, Vietnam and I could go on):

Let’s put that in growth numbers.

Two points to notice here:

pace has started to decelerate (natural path)

but the yearly additions in GW is now staggering. And for our investment purpose that is what matters

It is now a BIG market, growing by leaps and bounds annually.

That should be great for panel producers shouldn’t it ? Well, maybe soon but not yet …

HOW IS THE INDUSTRY STRUCTURED ?

The sector is roughly segmented in three parts:

Polysilicon making, the base material.

Ingot and Wafer (thin discs) makers.

And the final product, Cells (that get assembled into Modules/Panels).

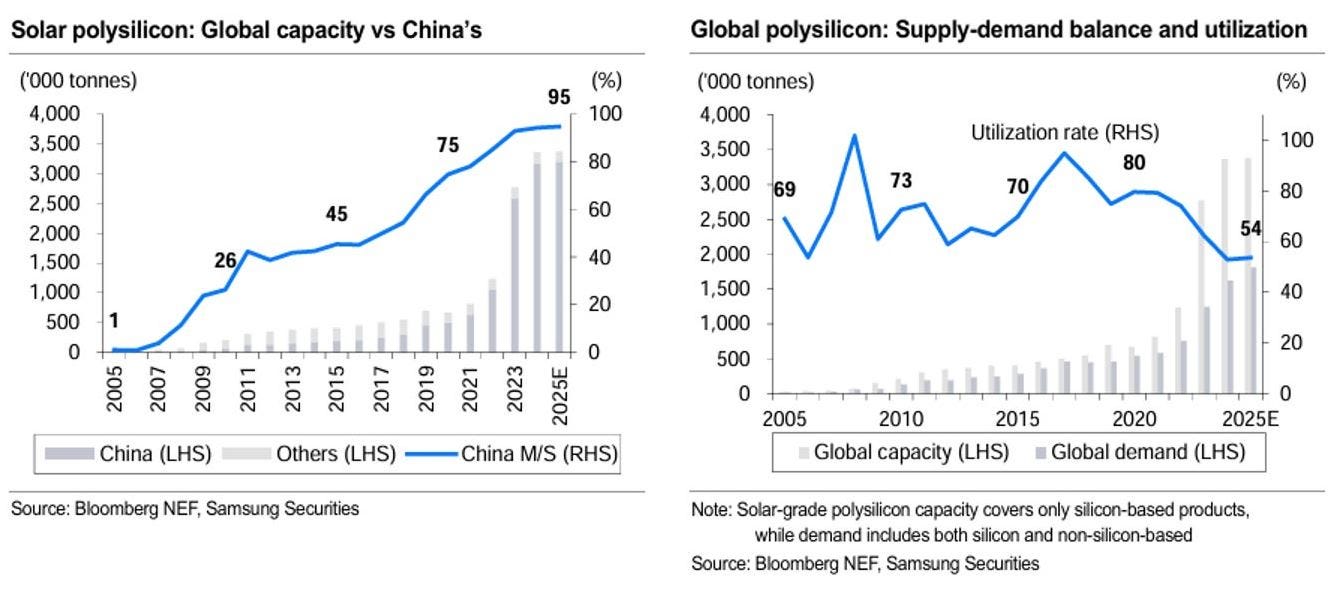

China completely dominates it: 90% of the polysilicon, 95% of the wafers and 80-90% of the cells and modules are manufactured in the Middle Kingdom.

China did not just became THE producer … it flooded the market:

Like other industries (automotive/EVs, lithium batteries), China has come to dominate the solar industry in the last 5 years and pushed it into oversupply territory.

Below is a picture of the Polysilicon market:

That obviously depressed prices.

So, as of mid-2024 when I first looked at it, the question was how long Polysilicon prices and cells would remain depressed for.

Nothing that was not seen before though. Polysilicon oversupply happened in 1988, 2003 and 2017.

It is a very cyclical industry.

And I like them: it creates investment opportunities for the “survivors” with the strongest balance sheet and best cash management.

2025, turnaround with policy intervention

A year after I started a position, China came with the catalyst I was waiting for: anti-involution policies.

This article from Deutsche Bank explains it quite well.

A number of producers in the Polysilicon solar industry segment, have started to actively phase-out capacity since Q3 2025. Plan is to shut 1/3 of capacity. And Polysilicon is seen as pilot for the other industries by the Chinese leadership. So there is political will behind it.

I think the market took notice.

Whether it is on Global Clean Energy (go back to chart at the top) or Solar segment (TAN ETF), a big trend change occurred in May/June of 2025, just before the Chinese leadership made those policies “a top priority” (see DB article, page 5).

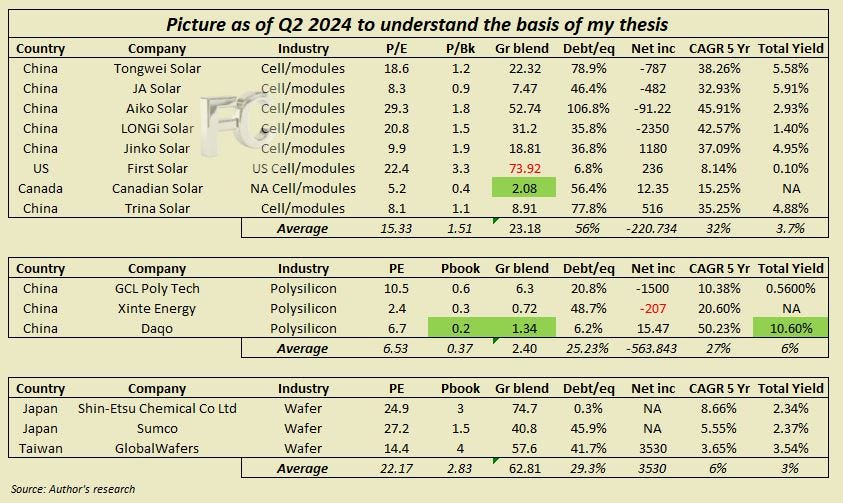

WHO ARE THE TOP PRODUCERS (largest by volume, from the top, per industry segment) with some financial metrics1:

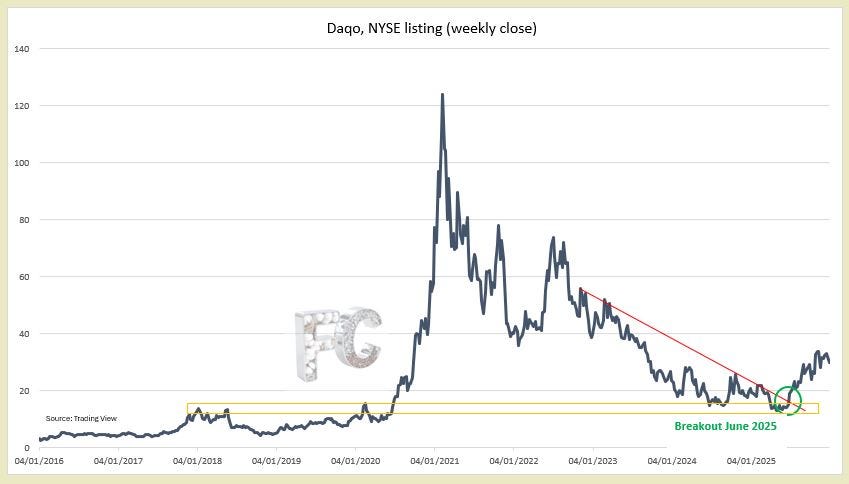

Daqo caught my eye.

- Super cheap (P/B)

- No debt

- High yield due to buybacks

It also has happened to pop on two of my screening tools (notably with one of the lowest price/book values in the world).

WHY NOT INVEST IN SOLAR PANEL MAKERS AND RATHER IN THIS OBSCURE SUB-SEGMENT ?

I am fairly flexible when it comes to allocating my investments.

But the basis is to control my downside.

I guess 15 years of prop trading Energy had its influence …

For me it’s all about risk/reward.

As long as I can control the downside, the upside should take care of itself.

It's not so far away from the concept of margin of safety from value investing advocated by Benjamin Graham. Just another angle to look at it.

One of the things that struck me on Daqo, was that the price it was trading at in Q2 2024 was much lower than its potential liquidation value.

I do follow, again, Graham’s framework, to calculate it.

Let’s be honest, it is very conservative2.

When I started buying in May 2024, Daqo was trading at 35% of its liquidation value …

It had NO long-term debt.

Here is an overview of how this metric stacks vs market cap over the last few years:

70-80% of their tangible asset value sits in cash and cash equivalents …

So, for me, this risk/reward meant that if it could avoid digging too much into its cash reserves in the next 12-24 months (time I asserted it could take to get out of the low part of the cycle, with polysilicon prices in the gutter), it would emerge with tremendous upside.

Again, the key would be: who is best placed to survive that difficult part of the cycle ?

Given how slowly Daqo was burning through its cash reserve, even after reaching record low Polysilicon prices, I think I had a good candidate3.

Let’s remember as well that in H1 2024 we were in the “non-investable” phase for Chinese assets.

I was told my valuation metrics (P/E and the like), and certainly my liquidation value exercise, would not mean anything when it comes to a Chinese equity.

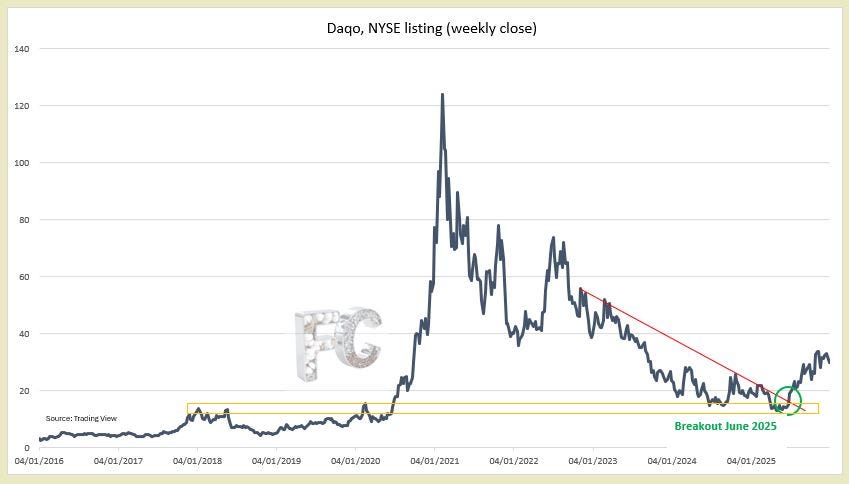

I think it has.

Unlike its closest competitor, Xinte, the share price has performed very well in 2025.

So maybe, it meant something after all …

Finally, I liked the behaviour of management. They triggered large buybacks (up to 11% of market cap) in 2024 to benefit from the dip and put some of their cash to use4.

There is a good chance they would do that again if we drop too much vs liquidation value. Again, controlling the downside …

CSIQ AS A HEDGE

As said, anti-China sentiment was rife in 2024.

And with Donald Trump rising in the polls in the second half, I got a bit worried about tariffs and full import restrictions on solar panels.

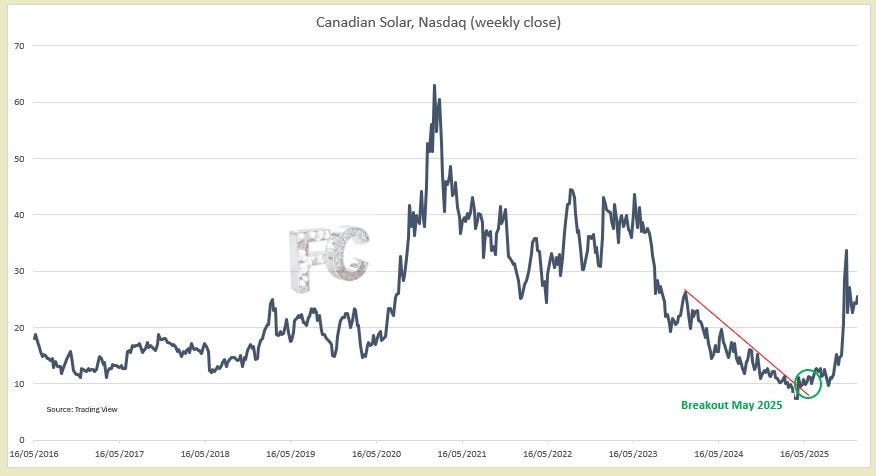

Given I had screened Canadian Solar to be one of the best “value plays” in the solar panels’ segment (i.e. Cells/Modules), which I had bought for a small position, I increased it thinking it could become a good hedge vs my Daqo position.

- as of Dec 2025 “Graham blend” (i.e. P/E time P/Book) is under 10. Vs 61 for First Solar.

- high short interest on the stock as of Dec 2025: 19.7%. I like this. It shows me there is a bunch of shorts to close if the industry recovers. I think it has shown in the price action in 2025.

CSIQ is present and expanding its production line in the US.

It allowed me to go up a bit more in the value chain, in a cell maker with decent value traits, unlike the rest of the sector.

Indeed, were it to be a favouritism of North American panel makers, First Solar and CSIQ could benefit greatly.

The former being too expensive for me, I increase my CSIQ position in late 2024.

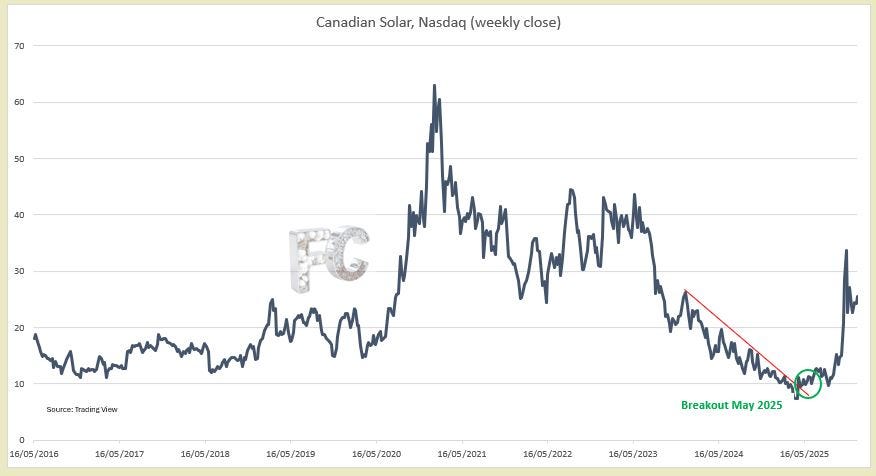

I don’t seem to understand that, even post tariffs, Canadian Solar has particularly benefited from a trend change in providers.

Rather, the whole sector took off. TAN ETF (Invesco Solar, listed on the NYSE) is after ICLN my second barometer for the sector:

Like ICLN, we broke the downtrend in place since 2021 in June 2025.

I used that to increase my position further in both stocks.

I think though that, maybe not because of tariffs (and they may well be reversed still) but because of the re-shoring trend, CSIQ has a great future tailwind behind itself.

RISKS OF INVESTING IN THE SECTOR

anti-involution policies completely fail:

we stay in overcapacity for too long and Daqo depletes its cash reserves. As calculated, that would take years … 4political changes across the board cutting new installations (notably in China but also Rest of the World) and killing the market. Very unlikely to be a problem even if it happens given the pace of additions.

Also, so far, despite big political changes in 2025 (notably in the US), it seems not to have put a dent in that trajectory.

Post-Trump election, US has seen 30 GW installed, on track for the largest yearly installation pace ever.investors start retreating (again) from China: 2025 was the start of international investors going back to China (I think it is only the start. I have much investment in China beyond Daqo).

If outside money were to step back alongside Chinese authorities’ attempt to revive their financial markets (which they actively do so) it would certainly hurt Daqo. Less so CSIQ.

I hedged quite cheaply the China risk in 2025.

Put options are even cheaper now on indexes (not Daqo itself), so one can easily hedge for instance a potential Taiwan conflict and roll that hedge every year (whether it’s on HSI Futures, or a broad traded ETF like FXI).

WHAT UPSIDE DO I SEE ?

Whilst I think in this new upcycle we could see EPS for Daqo going back in the 7 to 10 $ range, I will not base my profit taking on earnings’ forecasts and multiples.

Due to the nature of cyclicality of the sector, I will rather try to let run the trend now that we are in a new cycle. And see 2 to 4 years down the line where we are.

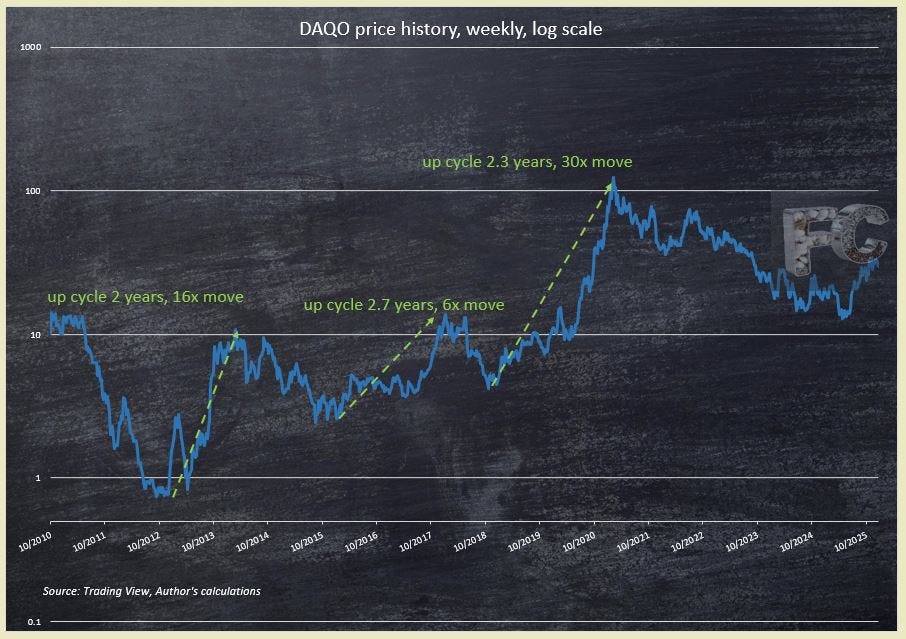

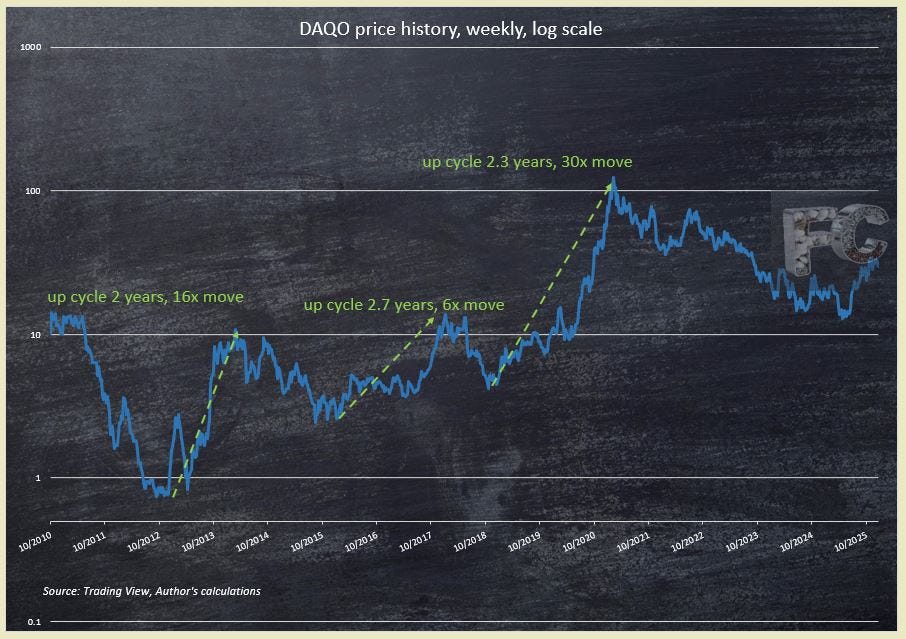

Past three upcycles returned 6x to 30x.

I think the upcycle could span longer than past ones though, given the large oversupply to tackle. Time length of the last downcycle also strengthens that view. Hence the 2-4 years target rather than 2-2.5 years.

Also, given the overcapacity, I would probably be happy to see P/Book and market cap vs liquidation value normalising to take some of the profits.

For Daqo it means the following:

- For a start, we are still trading at 70% of conservative liquidation value with no debt.

I would like us to go to a premium.

- On the Price/Book (see below), we are barely reaching the low end of the historical range taking out the extremes.

In an ideal situation it would go to 2 (upper bound of the red rectangle) and I would half my position.

But at minima I would like us to settle well within the rectangle to start taking some profits.

I may trade along the way.

And I will let the remaining position run for another 2 to 3 years from the beginning of 2026.

I would base my Canadian Solar position reduction off when I get out of Daqo.

I trade more actively on CSIQ though, and I took recently profits on some call options (see how steep the bounce was …).

If we correct deep enough I may re-enter some upside one year leap call options (we have now retraced 50% of the move so I am thinking hard about it).

I think it’s worth sharing the price action on this one given how abrupt it has been:

For good form, here is Daqo chart. Like CSIQ it may need to correct a bit more in the short term before the trend resumes. Either price wise, or time wise (ie sideway consolidation):

In conclusion, the sector has started to show some love in 2025 and the technical set-up is decent for it to continue in 2026 and 2027.

As always, remember the guiding light for your investments …

The D.Y.O.D.D. … Do Your Own Due Diligence.

The post is NOT financial advice, but rather to shine the light (sorry last pun !) on this previously hated sector.

Thanks for reading me

Fred

And feel free to ask any questions in the comment’s section. Happy to kick-off some discussions there.

That table contains a number of metrics I like to start with.

Price to Earnings ratio, Price to book, the multiple of both (I call it Graham blend for myself as it follows what he advocated in the Intelligent Investor), Debt to Equity ratio (I do also check interest coverage by Ebitda and current assets vs liabilities), Net Income, Revenue Growth over 5 years and Total Yield (ie dividend plus buyback yields).

It notably takes a 20% haircut on receivables, 35% on inventories and only take 15% (ie 85% cut) of the net property/other current assets and intangible assets.

At the low, Daqo was showing an average 65 M$ negative operating cash-flow per quarter. From their cash position of 2500 M$ to reach their market cap of 980 M$ it would therefore have taken 23 quarters …

I gradually put about 7% of my stock portfolio in it. An unusually concentrated position for me given I set at 3% large single equity positions.

But I spent so much time studying it and its market, again, I feel like the downside is controlled.

At what silver price would the solar makers find it difficult to earn a decent profit?

I’m also with Daqo, I think it’s the best prepared when the cycle turns around. In addition polysilicon prices have been increasing materially in the last months, so we might see Daqo breaking even in Q4 or Q1. Then on top it has a massive net cash position as you mentioned.