Mind the Gap

A Deep Dive into the London Property Market Correction

TDLR KEY TAKEAWAYS

1. A hidden but significant correction is underway

London residential property, especially buy-to-let flats, is experiencing a sharp and underappreciated price correction.

The move is visible on the ground (30–35% declines in some segments), even if it is not yet widely reflected in mainstream media or fully recognised by many investors.

2. The correction is driven by a combination of structural shocks

Four main forces are driving the downturn:

Rapid rise in interest rates

Outflow of high-net-worth individuals

Progressive tightening of UK landlord taxation

The Renters’ Rights Act, which triggered a rush for exits

3. The buy-to-let market is under forced liquidation pressure

A key dynamic is behavioural rather than purely macro:

This is not a normal cyclical slowdown.

4. This is a fear-driven dislocation that may create opportunity

INTRODUCTION

Unless you are actively following the London residential real estate market, you may be forgiven for missing the fact that the ground is “shaking” in this market.

It is not front-page news in the BBC or The Guardian.

Yes, there are occasional mentions of how difficult it has become to be a landlord, but far fewer references to how acute the price declines have been.

The average family in London has seen interest rates rise sharply and is feeling increasingly anxious about upcoming mortgage renewals. I see it around me. I hear it.

But even some of the more experienced local investors I speak with have, in some cases, missed the severity of the price trend that has developed over the past 12 months.

So, let’s dive in and look at similarities with other major global capitals, as well as the specific characteristics of the UK market.

QUICK GLIMPSE OF ARTICLES CIRCULATING RECENTLY

First, let’s acknowledge that an increasing number of articles in the press are now highlighting that significant changes are occurring in the market.

Here are a few recent headlines from major publications:

Most of this comes down to a new piece of UK legislation, the Renters’ Rights Act (link:).

It is a major UK law that overhauls the private rental sector by strengthening tenant rights and significantly restricting how landlords operate buy-to-let properties (ie investments).

It was originally introduced by the Conservative government under Theresa May in 2019, but only passed into law last year under the Labour government, and came into effect this year on 1st of May.

The main changes are:

Abolishes “no-fault” evictions (Section 21)1, widely seen as the most significant change

Replaces fixed-term tenancies with open-ended rolling contracts2

Limits rent increases (typically to once per year via a formal process)

Expands tenant protections and notice periods

Tightens rules on when landlords can regain possession

It is widely considered the biggest change in around 40 years, as it fundamentally shifts the balance of power toward tenants and removes key mechanisms landlords have relied on since the late 1980s.

CHARTFEST: LET’S PUT THAT IN PERSPECTIVE WITH HISTORICAL PROPERTY MARKET TRENDS

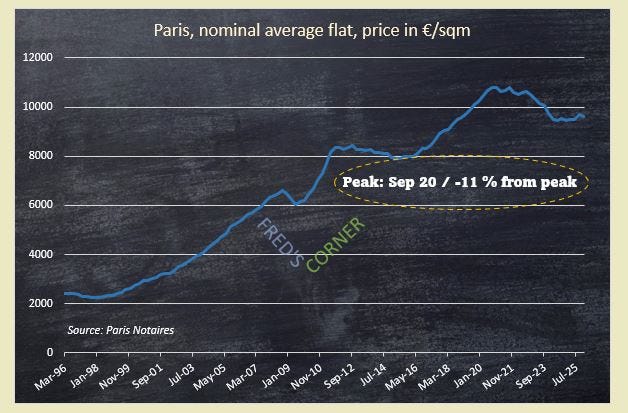

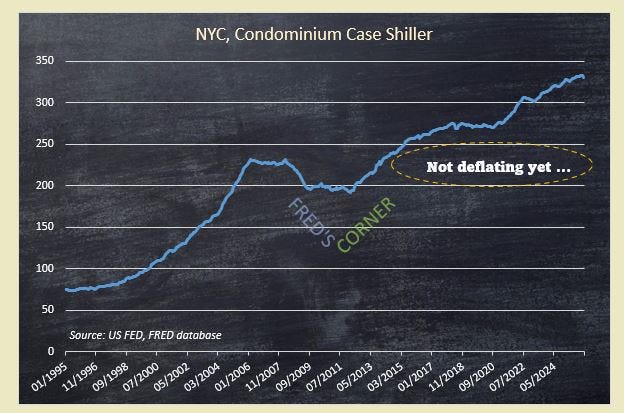

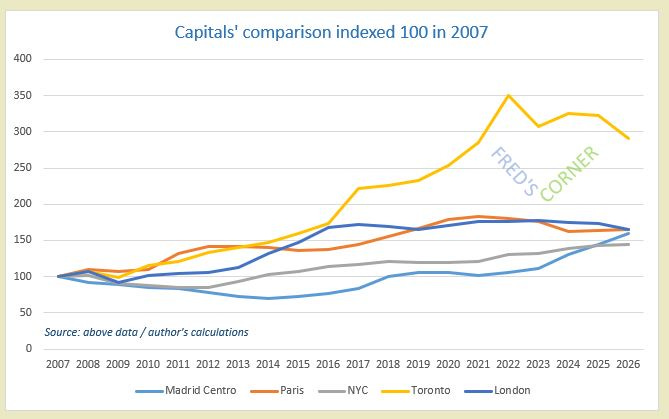

First, let’s look across the three main markets I track: London, Paris, and Madrid3.

To make it more inclusive and interesting, I am also including New York City and Toronto.

Geography is of paramount importance in property markets, so I acknowledge that New York is not necessarily representative of the broader US market at any point in time. But one has to make a choice.

Also note that these charts are useful to show trends and the magnitude of moves (notably recent percentage declines), but the underlying metrics differ:

London: prices in GBP

Paris and Madrid: prices per square metre in euros

New York and Toronto: index levels

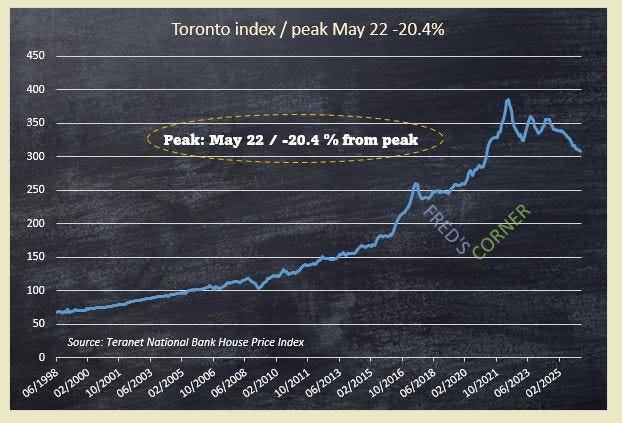

A sharp correction in Toronto.

New York City is not correcting… and Spain is still trending higher.

Now, if we index all of these markets back to 2007, we start to understand why:

We see a gradual convergence among the four major global cities (excluding Canada’s outlier position), with Toronto now adjusting down from what looks increasingly like an Icarus-style peak.

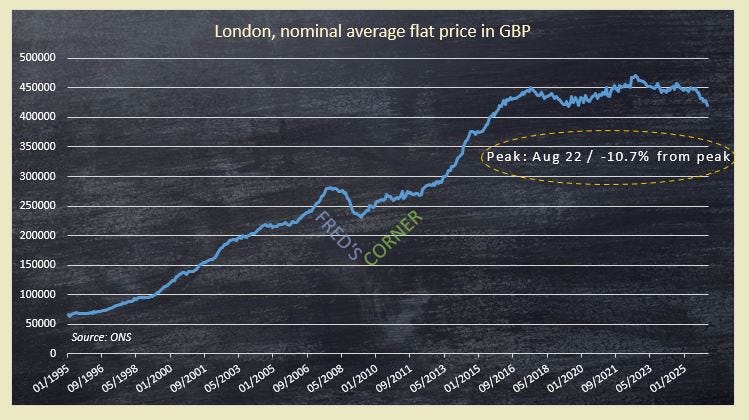

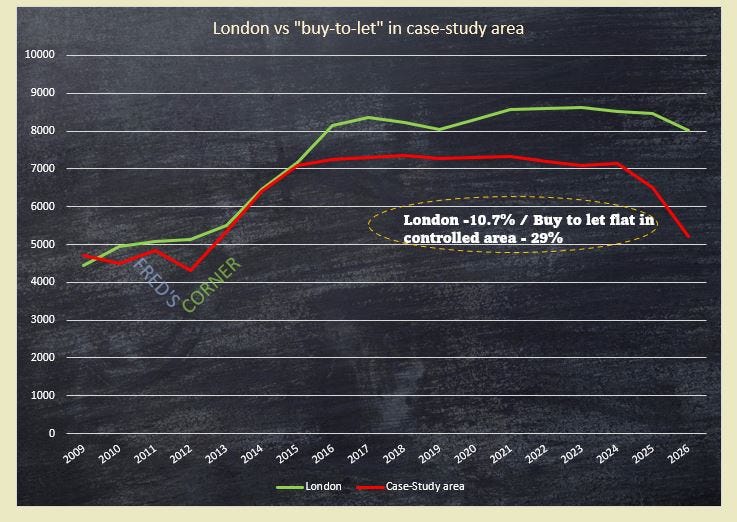

Now, the main motivation for writing this article comes from what I have observed on the ground in a number of “buy-to-let” flats, typically two-bedroom apartments, which represent the primary vehicle used by investors in residential property.

And the move since last year has been striking:

It has been literally tanking.

Now, the area I am referring to is my own local area in London. I know it quite well, as I have been tracking it since I bought my house here in 2009.

Even during the Global Financial Crisis, I did not witness a move like this.

If we compare it with other areas for which we have data, we get:

But it is not just in my area. In areas closer to central London, including one of the wealthiest neighbourhoods where my children go to school, I am seeing the same pattern.

And South-west of my location, in the immediate London suburbs where a friend is active in the market, the same trend is also clearly visible.

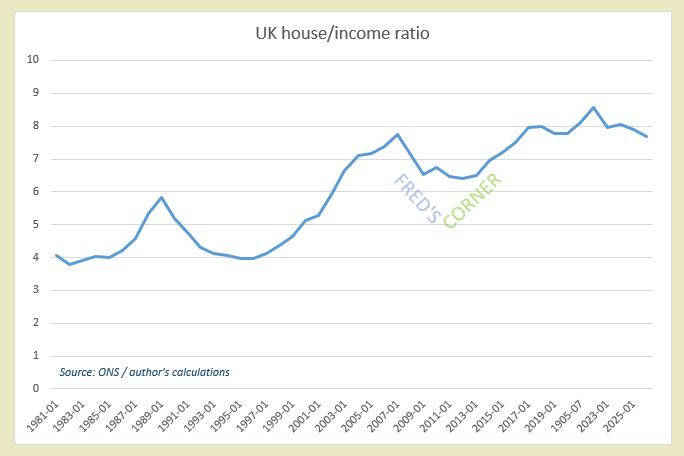

ADD-ON, CHARTS: PRICE-TO-INCOME RATIOS

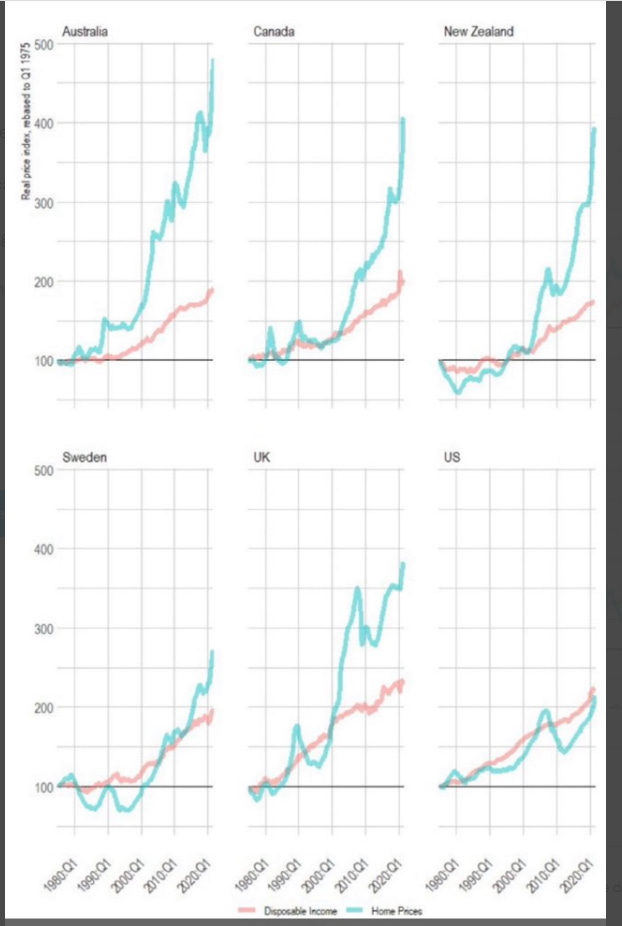

One of the most commonly used metrics in property analysis is the price-to-income ratio.

I particularly like the comparison below, originally produced in 2020, which spans over 40 years:

You can see how steep the increase in Canada and Australia/New Zealand has been.

This is also evident in the earlier comparison we made.

I regularly track and update the UK figures, and since Covid we have effectively plateaued and have now started to decline:

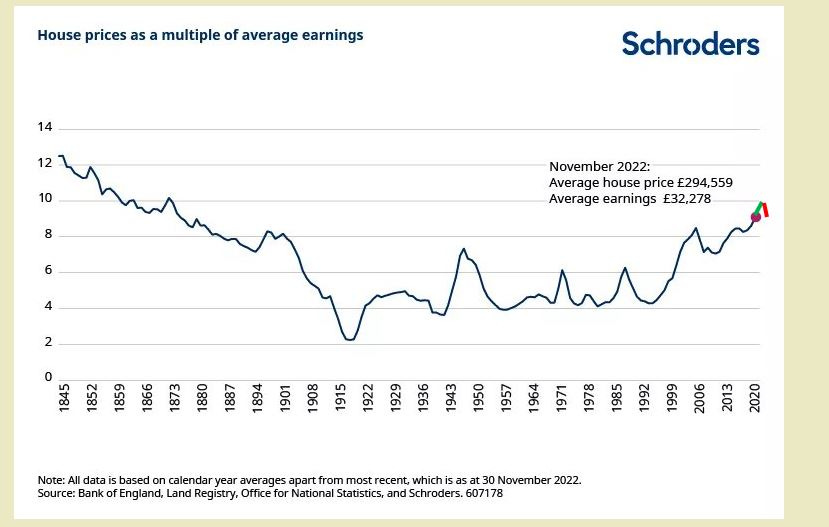

Now, one interesting data point from Schroders, the historic UK investment bank (which was acquired by a US investment group in 2026 after more than 200 years of independence), provides data spanning 175 years:

I have included my own update since 2020. As you can see, it does not really move the needle.

CAUSES OF THE “GLOBAL” CORRECTION

I use the term “global” deliberately, as I am hearing from various parts of the residential market, across the US (beyond just NYC condos, I believe), Canada, and Europe, that many regions are now experiencing corrections.

The first of the four main reasons why I believe it is fair to say that London is correcting is:

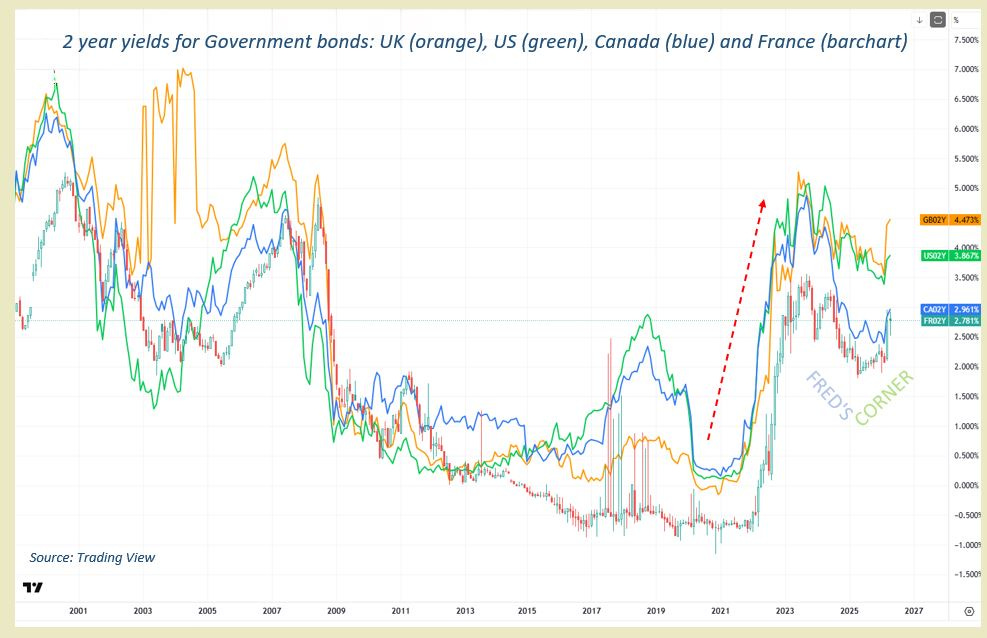

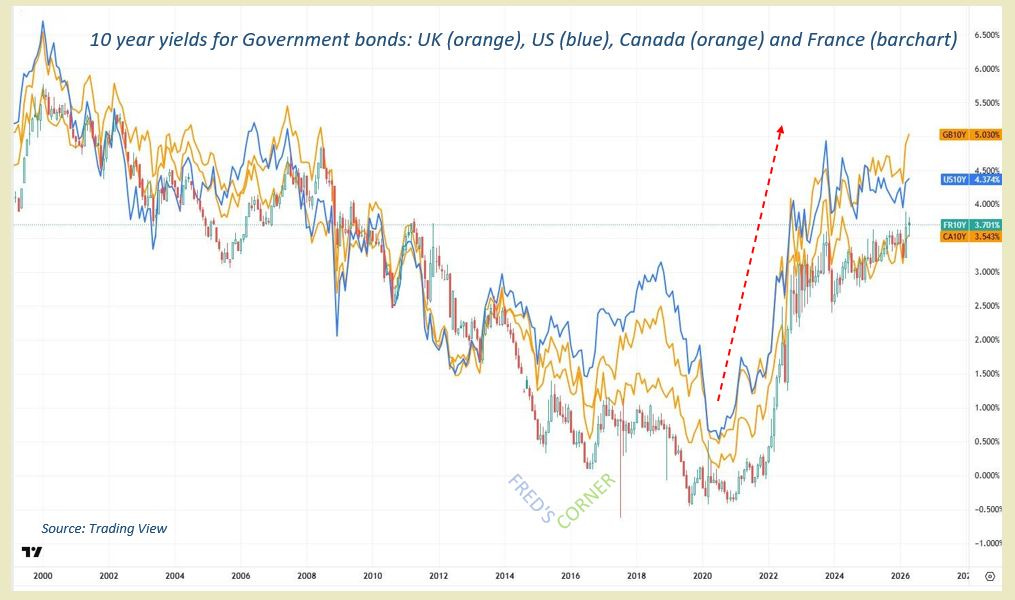

1. Interest rates: since the sharp rise in DM4 market interest rates in 2021-2022 , we have seen many property markets first slow down and then begin to correct.

Yields have indeed risen significantly across the board.

Let’s compare 2-year and 10-year government bond yields in Europe (I will use France as a proxy, as they are broadly synchronised), the UK (Gilts), Canada, and the United States:

After a 40-year downtrend in yields (broadly from around 1980 onwards), we have since Covid experienced a sharp rise in interest rates and bond yields.

Historically, this tends to put downward pressure on property prices.

As we have seen in Spain and New York City, this has not (yet) translated into clear price declines.

However, it has clearly had an impact in other markets, including the UK and London.

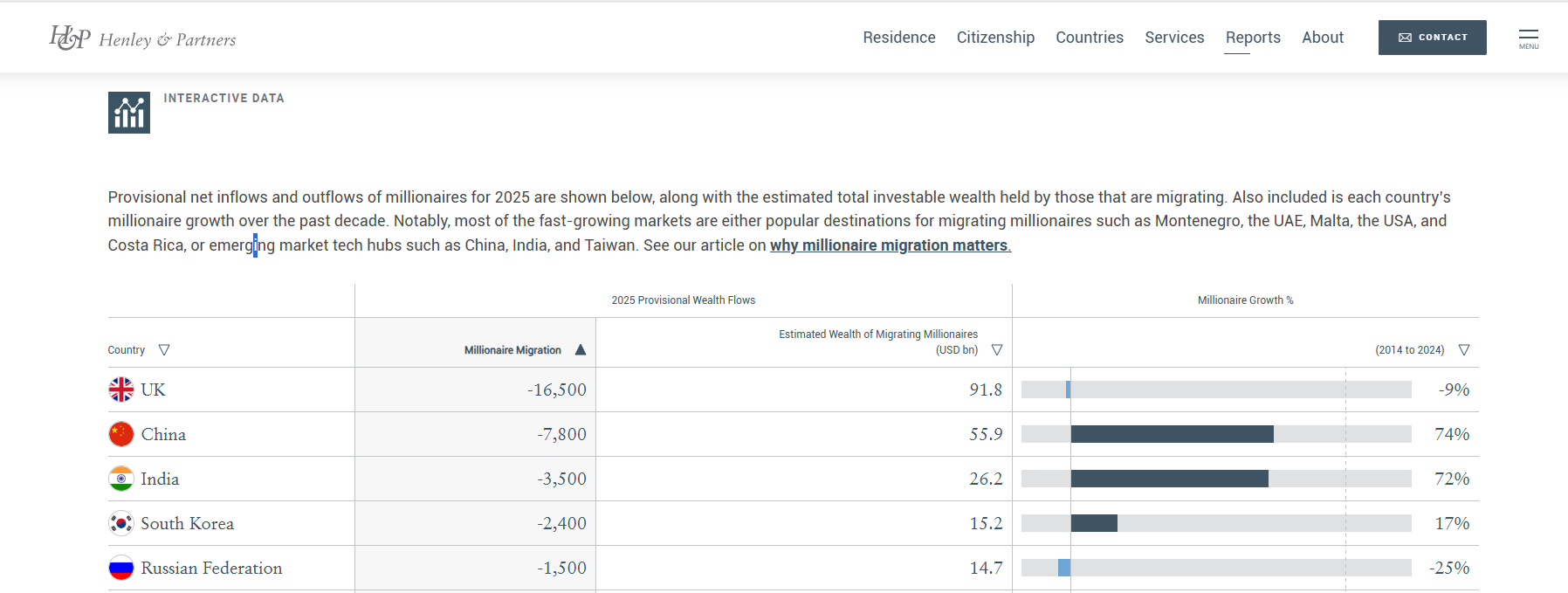

2. Outflow of High-Net-Worth individuals5 from the UK.

Following the Labour Party’s arrival in power, we have witnessed a notable outflow of high-net-worth individuals, driven in part (though not exclusively) by the removal of the UK “non-dom” status6.

This is visible in data from Henley & Partners, which shows that the UK was among the largest net losers of millionaires in 2025:

On the other side of the scale, destinations in 2025 were:

That cohort has underpinned the London property market for a long time.

Most notably at the very high end of the market.

But one should not underestimate its influence on the wider capital.

I have seen this firsthand since becoming a resident in 2005: Chelsea (on of the prime market) was gradually taken over by wealthy foreign buyers, who in turn pushed out less wealthy, but still affluent, residents. These households then moved one borough further out, which subsequently priced out long-standing local residents, and so on in a cascading effect.

We are now witnessing a significant correction in London’s high-end market, which is in turn spilling over into the broader market.

3. Increasing barriers to investors:

The UK has historically offered very favourable conditions for property investors, many of which have been gradually removed over time.

This is directly affecting the “buy-to-let” segment, i.e. the residential investment market, as investors slowly exit the system:

Landlords can no longer fully deduct mortgage interest from rental income (changes phased in between 2017 and 2020)

Increased taxation on property purchases for investors (notably the Stamp Duty surcharge on second homes)

Capital gains tax is becoming more restrictive, with lower tax-free allowances and higher effective taxation on gains from rental property disposals, as well as higher taxation on rental income overall

4. And finally, the recent major development: the Renters’ Rights Bill mentioned at the beginning

As explained in the first section above, this appears to be the final straw.

Beyond the price charts and the significant moves in the buy-to-let segment I mentioned earlier (with declines in the 30–35% range), it is worth briefly expanding on what is actually happening on the ground.

The best analogy is the “narrow exit door”.

As the law was expected to come into effect on 01/05/2026, “investor landlords” (notably in the 1 to 3 bedroom flat segment) have gradually, and then suddenly, all rushed toward the exit at the same time.

This has crowded the market, and over the past 10 months (starting in summer 2025), that segment has come under increasing pressure.

My letting agent, who normally finds tenants for the house I own just down my road in a very popular neighbourhood, told me that from October to the end of March (when we last spoke), around 90% of his time had been devoted to sales rather than lettings.

Let me repeat that: an agent who normally focuses exclusively on rentals has been asked by his clients to dispose of their portfolios, and that is effectively all he has been doing for months.

We are mostly talking about individuals who have inherited rental portfolios rather than actively built them. They are sitting on relatively comfortable assets yielding 3–5%.

Now they all want to sell. And sell everything at once.

To be clear, in my view, the Renters’ Rights Bill is simply the straw that broke the camel’s back. It is amplifying fear in the market, but it comes on top of the structural pressures mentioned earlier.

And that point is important: there is currently a significant amount of fear in the market.

I will come back to this later, as, being naturally contrarian, I see opportunity emerging from this.

ONE MORE CHARACTERISTIC OF THE UK PROPERTY MARKET

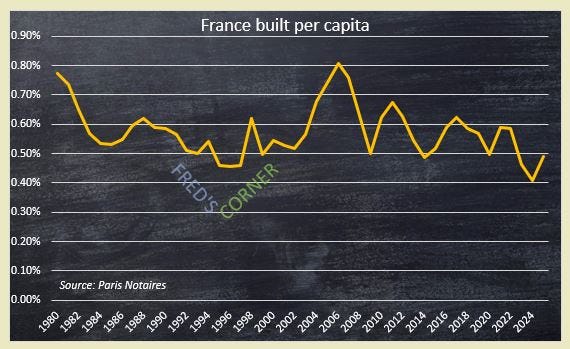

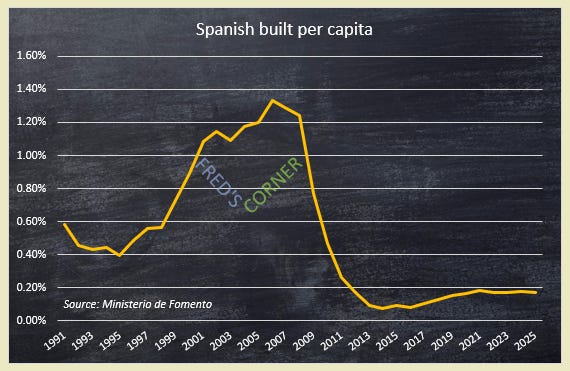

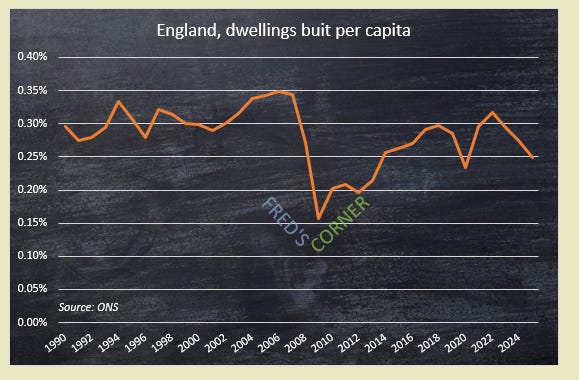

Across my three core markets—UK, France, and Spain—I like to track another indicator: the level of new housing construction per capita.

In all three countries, I have heard for more than two decades that the housing crisis is a major concern and a central topic in political debate:

Specifically in the UK, planning permission is widely seen as a major bottleneck preventing higher levels of construction.

Local authorities are often viewed as constraining national housing ambitions set by political leaders. The system itself is legally complex, slow, and highly risk-averse. I had even considered undertaking a property development project myself, but after speaking with several developers and architects, I concluded that the risk/reward in the UK is simply not attractive enough.

This is reflected in the number of dwellings built per capita.

Here is the comparison across the three countries:

Spain had a massive overhang following the Global Financial Crisis, with an extraordinary number of properties built during that period.

However, the UK, on average, and at its current level of construction, is still far behind France, which itself is facing its own housing supply challenges.

We are currently building in England only around 50% of the number of dwellings built in France.

This chart made headlines in the Financial Times a few months ago. In their calculations, the UK situation appears even worse…

TAKEAWAY #1: NEVER SAY NEVER

Quoting once again my risk management, and more broadly my investing mantra: Never say never.

I did not expect to see a deep property price correction comparable to what I observed during the Global Financial Crisis.

The UK is currently near its highest employment levels in 50 years.

We are not facing a global financial crisis (although there is clearly an interest rate issue).

Yet the price declines we are experiencing are gradually approaching, on average, the magnitude of what occurred during the GFC, if the current trend continues.

More importantly, in many parts of the buy-to-let (investment) market, that adjustment has already effectively taken place:

I was considering adding to my portfolio (in a contrarian move) a year and a half ago. Given the type of financial market environment we have been seeing, I assumed I would have no opportunity to do so (after all, most equity indices are at or near all-time highs).

Yet here we are.

And this is striking when looking at long-term charts. Historical drawdowns tend to appear shallow and recover relatively quickly. The current stress in the market is therefore clearly visible, even on a long-term lens.

TAKEAWAY #2: POTENTIAL OPPORTUNITY

Remember the agent I mentioned earlier. He has been asked by his clients to offload entire portfolios.

He could comply, take a good commission, find new buyers, and continue managing the rental stream as before.

Instead, he has been trying to convince them to hold, arguing that the new legislation is not, in itself, a barrier to renting.

I tend to agree, and I believe this represents a genuine opportunity.

Large price corrections in buy-to-let (investment) flats are not common. They are currently offering attractive yields, around 7–8% gross in many cases.

However, there are still several constraints:

High service charges (the equivalent of North American HOA or condo fees), which make some investments difficult to justify

Higher and more volatile interest rates, which complicate financing decisions

Broader affordability issues (as reflected in price-to-income ratios), which make me reluctant to rush in

There is a significant amount of fear in this market, and part of it is linked to the current political environment.

However, Labour will not remain in power indefinitely, and I expect investors to return over time.

There is no free lunch, but with some work, I believe opportunities are emerging. I expect a degree of normalisation over time (i.e. prices reverting upward from current levels), particularly in an inflationary environment.

To me, the value is compelling—especially when compared with other European capitals. The key challenge is making the rental yield work, which is currently more difficult due to high financing costs and competition from government bonds (Gilts).

As a result, I am approaching the market selectively.

CONCLUSION

I believe there is a clear opportunity to step back from fear and selectively look at the buy-to-let (investment) segment, i.e. 1 to 3 bedroom flats in London.

This is not a timing call, and it is important to remember that this is a structurally slow-moving market.

I am simply highlighting what I consider to be a historic price correction in one segment of the market.

In the broader UK and European property market, if interest rates remain elevated and more homeowners refinance at higher levels in England, conditions could deteriorate further.

We will also need to assess the true impact of the Renters’ Rights legislation later this year, which is likely to act as a continued headwind.

As always, remember the DYODD

Do Your Own Due Dilligence !

Thanks for reading,

Fred

Section 21 (often referred to as a “no-fault eviction”) was a UK rule that allowed landlords to evict tenants at the end of a tenancy without giving a reason, provided the correct legal notice procedure was followed.

This mechanism was widely used as part of a standard legal framework to end tenancies before starting new ones (with either the same or new tenants).

The UK rental market traditionally operated mainly through ASTs (Assured Shorthold Tenancies), which typically had fixed terms of 1–2 years (or longer). This is now changing, and landlords will instead need to rely on open-ended tenancies, with tenants remaining in place until they choose to leave (with two months’ notice).

Landlords will only be able to repossess properties under a limited set of conditions, including notably:

tenant rent arrears

intention to sell the property

intention for the landlord (or close family member) to move back in

I am trying to remain consistent in listing capitals, but my primary interest is in Catalonia in Spain, specifically Barcelona, rather than Madrid, based on personal preference.

DM: Developed Markets refer to countries whose economies are considered highly mature, stable, and industrialised, with strong institutions, high income levels, and deep financial markets.

HNW: High-Net-Worth individuals: people with a large amount of investable assets, typically excluding their primary residence.

Non-dom status in the UK refers to “non-domiciled” tax status, where individuals living in the UK were taxed differently on foreign income and capital gains depending on their domicile (i.e. their permanent home country).

It allowed certain UK residents to avoid paying UK tax on foreign income unless it was remitted (brought) into the UK.

It was highly advantageous for very wealthy individuals and made the UK a long-standing hub for global wealth.

British millionaires in UAE are now caught between missiles from Iran and high taxation from UK!

Interesting topic. I read a paper a while back (when I was looking to buy my house) that tried to compute fair values for properties in G10 countries based on the following variables: multiple of yearly avg rental income potential + closeness to downtown core + closeness to public transportation + new construction of the property type (detached, semi, or condos). Wondering if a fair value property index/estimator would be interesting. There may be something like this; I am not particularly plugged into the property market investing space, so I don't know.