China: Value in Exile

When Great Companies Trade at Unfashionable Prices

TDLR Key Takeaways

1. China remains structurally under-owned vs its global importance

Despite being a major global economic power, Chinese equities represent only a very small share of global investor portfolios, creating a potential long-term allocation gap.

2. Sentiment has been extremely negative, but fundamentals are improving

After years of regulatory pressure, property stress, and weak growth, parts of China’s economy and technology ecosystem are showing signs of stabilisation and renewed innovation strength.

3. Valuations are at a major discount relative to history and other markets

Chinese equities (especially tech) remain among the cheapest major markets globally, with Brazil also standing out, while US valuation expansion has been driven largely by earnings upgrades.

4. A re-rating could be driven by capital flows and policy shifts

Historical precedents (Japan, South Korea) suggest that governance reforms, buybacks, and capital allocation improvements can trigger re-ratings, something China has started to replicate, even if global investor participation remains low.

INTRODUCTION

I first became a big fan of Chinese equities in 2022.

Alibaba, which I had been tracking for some time, was in freefall and had fallen 78% from its Q4 2020 peak.

Chinese regulators had cracked down on a number of technology companies. Chinese ADRs were facing delisting risks, and the country’s strict Covid lockdowns were fuelling concerns among international investors.

In March 2022, analysts at JPMorgan Chase famously described China as “uninvestable”, prompting a number of institutional investors to publicly argue that the market should be avoided altogether.

Things were not much better in 2023. Economic growth remained weak and the property sector was in full crisis mode.

Yet the more I looked at China, the more attracted I became.

As readers of my previous articles will know, I like a good bargain, and valuations looked remarkably cheap across many parts of the market. In fact, Chinese equities as a whole were trading at some of the lowest valuation levels in the world, both relative to other major markets and to their own history.

The wait was long and often painful, but 2024 proved rewarding, and my main technology investment reached its target in 2025.

Since then, Chinese equities have corrected once again, while other technology-heavy markets (most notably the Nasdaq, but also South Korea) have continued an almost relentless bull run.

I believe it is time to take another look at China, its technology sector, and whether the opportunity remains compelling enough to dip our toes back into the water, or, in my case, increase existing positions.

MACRO BACKGROUND

There is another reason why I have been a long-term fan of China.

I am attracted to major secular trends and long-duration investment themes.

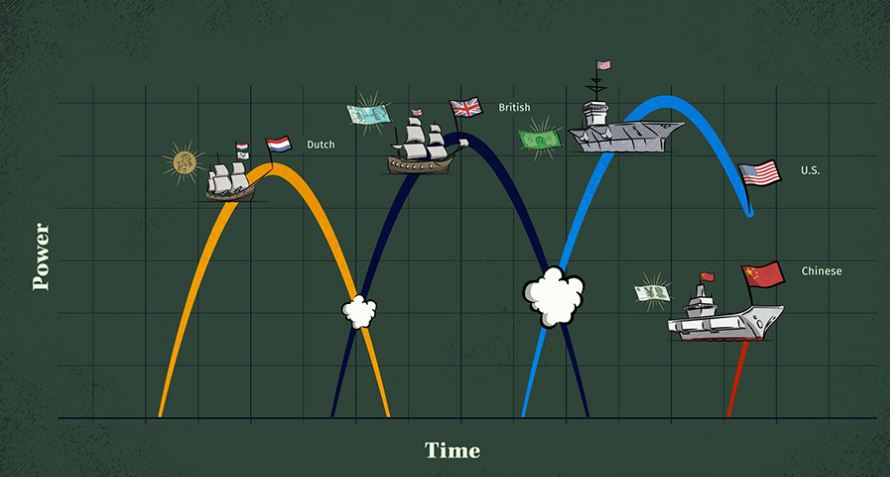

One framework that has resonated with me is the one developed by Ray Dalio in Principles for Dealing with the Changing World Order (2021). The following link provides a useful summary of some of the book's key concepts and accompanying infographics:

Dalio’s central ideas can be summarised as follows:

Great powers rise and fall over decades, not years.

Regardless of one’s political views, history suggests it is difficult to stop a country once it has reached superpower status.

China has crossed important thresholds in areas such as education, technology, trade influence, and manufacturing capacity.

I am fully aware of the challenges the country faces.

The most important factor may be demographics. As we will discuss in a future article, however, demographics are not everything. Japan, for example, has one of the most challenging demographic profiles in the developed world, yet its stock market has performed exceptionally well in recent years.

China has also been dealing with a severe property-market crisis and may still face elements of a balance-sheet recession similar to those experienced elsewhere in history.

Yet the bullish macro case has arguably strengthened since I first read Dalio’s book.

China continues to expand its sphere of economic and technological influence:

The country overtook Japan in 2023 to become the world’s largest automobile exporter.

Artificial intelligence: the emergence of DeepSeek surprised many observers and demonstrated that China remains capable of producing world-class AI models and innovation.

Patents: BYD is a fascinating example. The company has filed more than 50,000 patents across a wide range of technologies, including electric vehicles, batteries, electronics, energy storage, and manufacturing processes. In electric vehicles alone, BYD has reportedly filed more than 15,000 patents, many times the number attributed to Tesla.

Renewable energy: China has dramatically accelerated its deployment of renewable energy infrastructure, battery production, and associated supply chains, as discussed in a previous article.

Biotechnology and robotics are increasingly becoming areas in which Chinese companies compete at the global frontier.

The country now operates by far the world’s largest high-speed rail network.

Taken together, these facts on the ground make it difficult for me to ignore the opportunity.

I appreciate that discussions about China can sometimes become politically charged. My objective here is not to make political judgments but to analyse investment opportunities. As investors, our job is to observe reality as it is, assess the facts objectively, and allocate capital accordingly.

GLOBAL ALLOCATION: ANOTHER REASON TO BE PRESENT

Combining all of the above, my view is relatively simple: if there is a reasonable chance that a country could become the world’s largest economy (or remain one of its two dominant economic powers) it probably deserves a place in an investor’s portfolio.

That does not mean it should represent the majority of one’s holdings.

But it arguably should not be zero either.

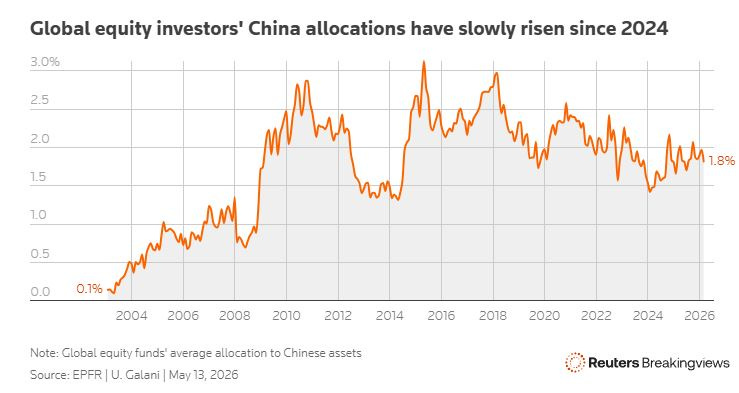

Yet, during the depths of the pessimism in 2022–2023, some estimates suggested that international investors’ average allocation to Chinese equities had fallen to just a few percentage points of their portfolios.

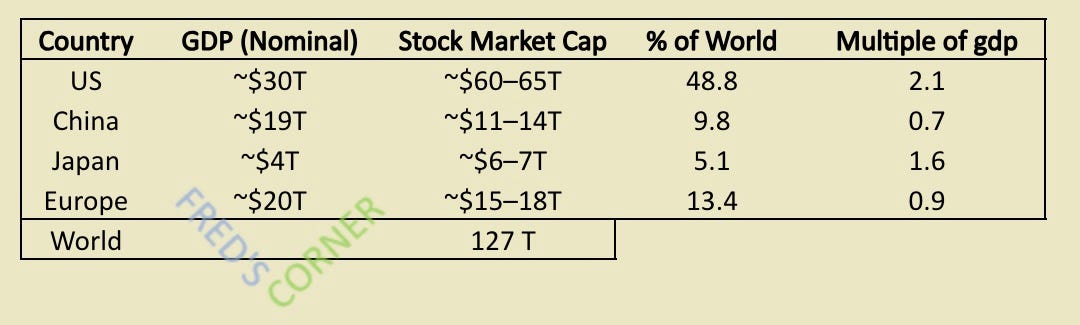

When we compare the relative size of China’s economy and capital markets to the allocation it receives from global investors, the picture is quite striking:

If we compare the relative size of global stock markets, the picture is quite striking:

I am of the opinion that for Chinese equities to deliver truly exceptional returns, one or both of the following developments will likely need to occur:

Chinese households redirect a larger share of their substantial savings into domestic equity markets.

International investors increase their exposure and return to the market in meaningful size.

In both cases, regulatory and policy changes could act as important catalysts.

Japan provides a useful recent example. Beginning in 2023, a series of reforms helped reignite investor interest and contributed to a powerful rally in Japanese equities:

The Tokyo Stock Exchange began pressuring undervalued companies1 to explain how they intended to improve capital efficiency and shareholder returns.

This encouraged a significant increase in share buybacks2 and corporate restructuring.

Long-standing cross-shareholding arrangements between large corporations were gradually unwound, helping to unlock value.

Improvements in corporate governance standards increased investor confidence and market transparency.

A similar story unfolded in South Korea through the Corporate Value-Up Programme launched in 2024.

The initiative sought to improve shareholder returns, strengthen corporate governance, and encourage better capital allocation. Combined with the strength of the semiconductor sector, these reforms helped drive a significant re-rating of Korean equities.

China is not Japan, nor is it South Korea. However, these examples illustrate how policy changes, governance reforms, and shifts in investor behaviour can materially alter market valuations over time.

For a market that remains deeply out of favour with many international investors, even modest improvements in these areas could have a meaningful impact.

NOW, CHINA HAS STARTED TO MOVE IN A SIMILAR DIRECTION.

Recent initiatives include:

In late 2024, regulators introduced market value management guidelines encouraging listed companies, particularly large state-owned enterprises, to place greater emphasis on shareholder returns.

The Shanghai Stock Exchange launched its “Corporate Value and Return Enhancement” initiatives, aimed at improving capital allocation and investor confidence.

Companies have begun responding, with share buybacks reaching record levels in 2024.

So far, however, global investors remain focused on the risks discussed earlier, as well as perhaps the largest one of all: geopolitical risk.

Ultimately, views on that risk will vary from one investor to another. My own view is that, from a diversification perspective alone, China deserves a place in a globally diversified portfolio.

And probably a larger one than the roughly 1.8% allocation to Chinese equities reportedly held by international investors, according to Reuters.

THE VALUATION GAP

Despite everything discussed above, valuation remains the primary driver of my investment interest.

Indeed, it is one of the main reasons I have devoted so much time and capital to Chinese-related investments over the past few years.

China has been (and despite the recent rebound, arguably still is) one of the cheapest major equity markets in the world.

To me, that has simply been too compelling an opportunity to ignore.

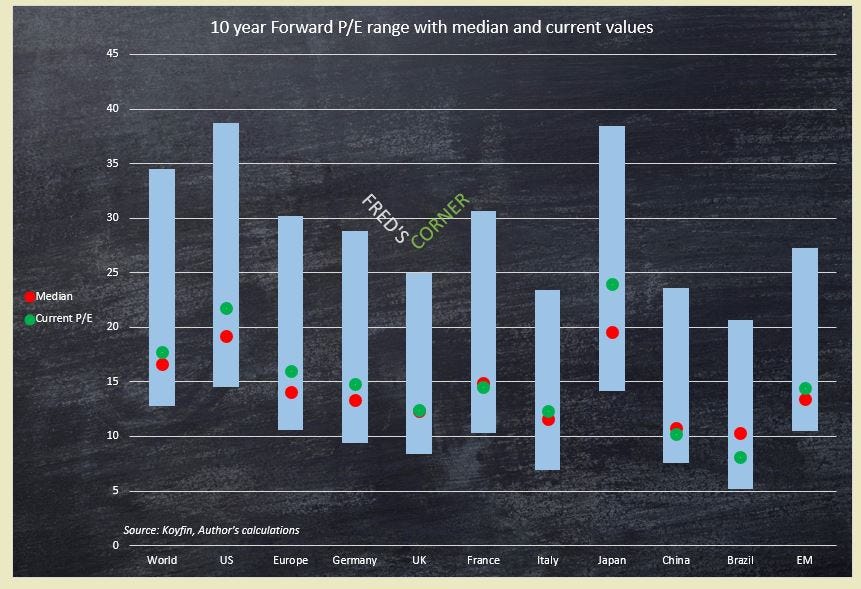

Looking across global equity markets today, the valuation picture remains striking:

Note on Forward P/E here3

China and Brazil stand out as particularly inexpensive markets.

Given the macro tailwinds for China discussed earlier, the combination of strong long-term fundamentals and attractive valuations makes a compelling case for maintaining a meaningful allocation.

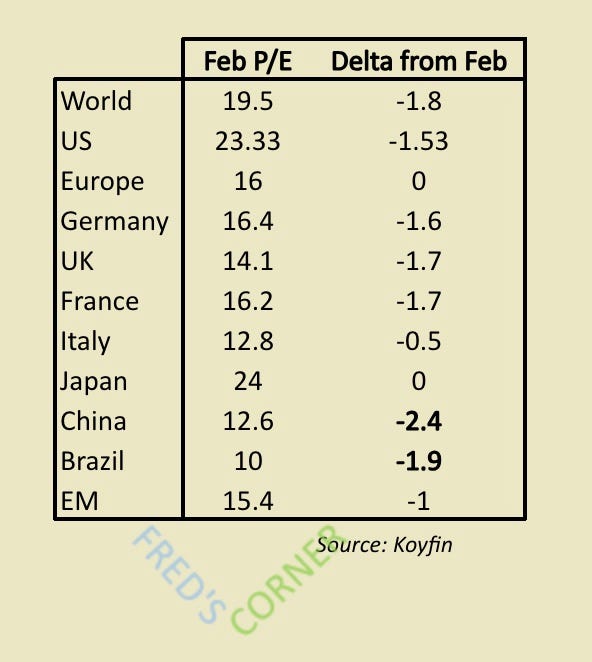

If we compare current valuations with those from earlier this year, P/E ratios have compressed further since I wrote about Brazil in February:

As we can see, Brazil (and even more so China) stand out as having experienced some of the largest valuation corrections.

In the case of the United States, most of the recent P/E compression has come from earnings estimates being revised higher. Despite the market rising roughly 10% since February, valuation multiples have actually declined.

China and Brazil present a different picture. Their equity markets have fallen approximately 9% and 11% respectively, while earnings expectations have also improved. As a result, valuations have become even more attractive.

WHY NOW ?

I reduced one of my larger Chinese technology positions last year after it had appreciated very rapidly and reached my target.

I also reduced risk more broadly following the outbreak of the Iran conflict.

Since then, however, several of the Chinese charts I follow have corrected significantly, while many of the world’s major equity indices have continued their powerful advance.

That divergence has caught my attention.

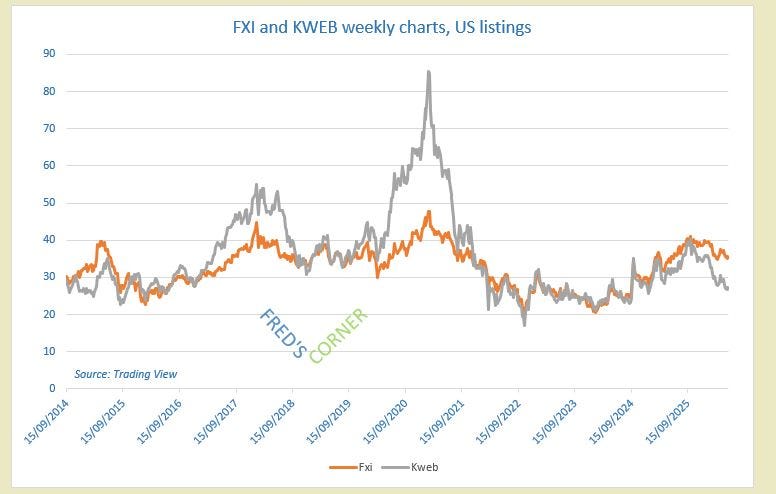

Let’s start by looking at two of the main China-focused ETFs trading in the United States: FXI and KWEB4:

Beyond the very large correction in Chinese technology stocks since 2021, two additional points stand out:

The downtrend that began in 2020/2021 was broken in 2024, suggesting the market may have entered a new phase.

However, prices remain far from making new all-time highs, very much in contrast with US indices.

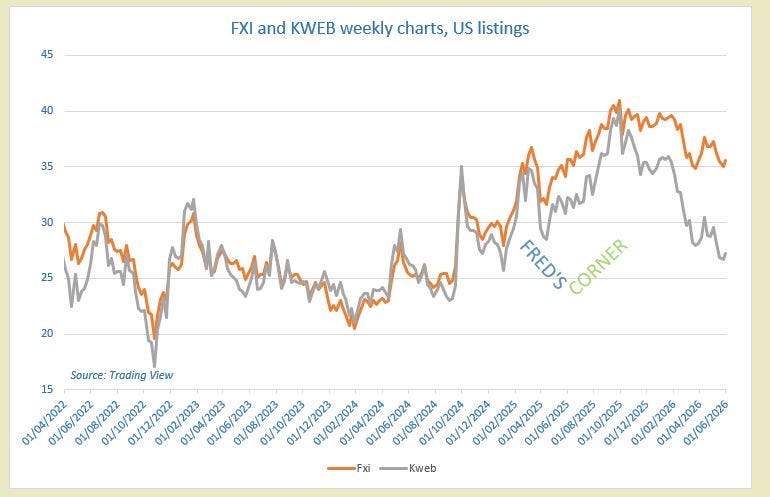

If we zoom in starting from the 2022 lows:

The underperformance of KWEB (the main US-listed Chinese internet/tech ETF) remains striking.

Given that I still like several of its underlying components and want exposure to the theme, I have begun gradually rebuilding the long position I had reduced in Q4 last year.

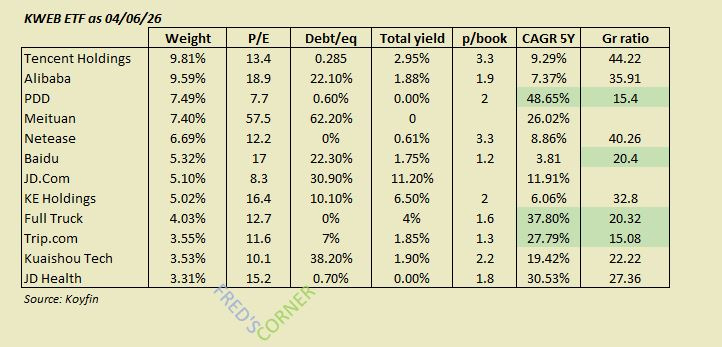

From a valuation perspective, the top 12 holdings of the KWEB ETF (representing approximately 70% of the fund) currently look as follows:

The weighted average for the ETF as a whole provides the following approximation:

Not cheap in absolute terms, but for a technology-focused group with approximately 47% average annual revenue growth, I find it attractive.

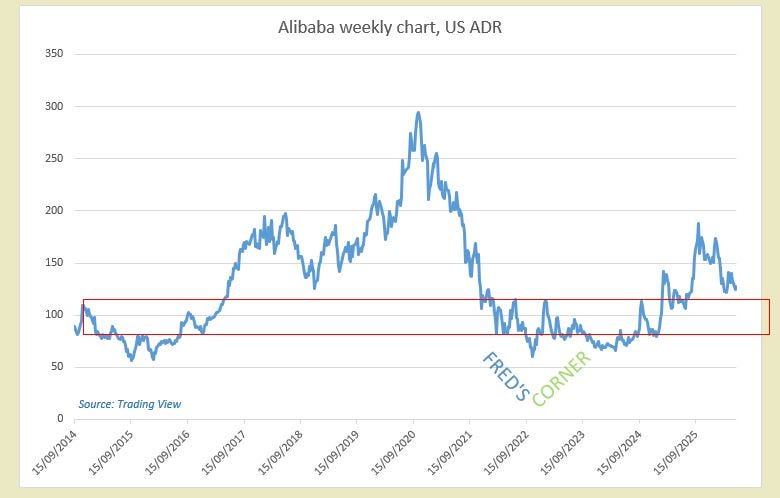

One stock I have been actively trading and investing in is Alibaba.

Back in 2022–2023, the company reached a point where roughly half of its market capitalisation was represented by net cash. At the time, I built a significant position.

The historical chart looks like this:

The bottoming formation in 2023–2024 appears relatively clear to me.

As we approach the upper boundary of the recent consolidation range (highlighted in red), I am becoming interested again. I am still waiting for slightly more confirmation, as the daily chart is not yet entirely clean, but I have started to gradually rebuild a position after having exited approximately two-thirds of my holdings when the stock reached my target range of $180–185 last year.

Finally, one additional chart that I think is particularly relevant in the context of the broader fundamentals discussed earlier is BYD.

As mentioned previously, I believe the company is a leading candidate to become a global leader in electric vehicles.

A couple of years ago, conversations I had with European and US investors tended to focus almost exclusively on Tesla. The real growth in “emerging” markets was far less appreciated. Yet on the ground, in places like Brazil, BYD vehicles were already highly visible. More recently, I have started to see a similar trend in the UK, and I do not expect that to reverse.

Beyond electric vehicles, BYD also represents a highly capable innovation and manufacturing platform.

Valuation-wise, the stock is not cheap at around 30.3x forward earnings. However, with revenue growth of approximately 38.7% CAGR over the past five years, it is not obviously expensive either.

Anyway, here is the chart:

If my approximate trendlines are indicative of a new, very wide trading range, then we are not far from the lower bound.

That said, I also believe (although this is clearer on the daily chart) that the downtrend in place since 2024 has been broken.

Once again, I am gradually building a position.

CONCLUSION

I want to emphasise my usual disclaimer: this is not financial advice.

I have touched on a number of fundamental drivers, valuation metrics, and technical levels, but readers should always conduct their own due diligence.

The examples discussed above represent only a subset of the major listed companies in China. Tencent, for instance, is another major technology behemoth alongside Alibaba and may be preferred depending on individual investment preferences.

It is also important to stress that this analysis only scratches the surface. A simple global screening exercise shows that Chinese equities frequently rank among the cheapest markets globally, with many companies trading on low price-to-book multiples, minimal leverage, and in some cases net cash balance sheets5.

At current US valuation levels, China increasingly looks like a “value outlier”, or at least a region that could attract meaningful capital flows as global investors gradually reconsider allocations away from markets that have experienced strong multi-year performance, such as the US and South Korea.

As always, remember the DYODD

Do Your Own Due Dilligence !

Thanks for reading,

Fred

those with price to book below 1

When a company buy back its own share, reducing the sharecount and mathematically increasing the valuation ratios like price to earnings for instance.

Forward P/E: is a valuation ratio that compares a company’s current share price to its expected earnings per share over the next 12 months.

FXI: iShares China Large-Cap ETF

KWEB: KraneShares CSI China Internet ETF

A net cash balance sheet is when a company’s cash and liquid assets exceed its total debt, meaning it has more cash than financial liabilities.

Thank you for this very revealing post. There is absolutely no speculation in China assuming the pre eminent role in research and develolment, at least in my field. In every AI conference (e.g. the recent CVPR edition at Denver) one will find that about 60% of the attendees are Chinese. Paper acceptance is entirely based on merit. When the Chinese portion dominates, we can extrapolate so many things - the funding, the research capital being built and the inexorable nature of china's rise as a technological superpower.

Hi Fred, I cannot buy KWEB on my French broker so I use HSTE.PA to get exposure to these Chinese dragons. The index is Hang Sen Tech. So far I'm 20% in the red but I have angelic patience.